In today's volatile economy, credibility is a real issue for banks. Financial institutions feel a constant pressure to regain and improve customer satisfaction and trust.

With so much transparent content being generated through social media each day and with rapidly evolving technology, financial institutions find it increasingly more challenging to deliver a consistent and integrated customer experience.

Many brands in other industries have discovered several creative ways to use social media to solve customer issues and keep all members apprised of important information.

So why isn't this always the case yet in the financial industry?

Last week, we hosted a casual, peer-to-peer discussion on today's challenges and the future of financial services and social media. We were fortunate enough to be joined by 4 panelists with experience in scaling for social at major financial brands.

There were some fascinating debates and lots of practical examples of how banks, credit unions and insurance companies have made best use of social media.

For those who weren't able to attend, you can find some good examples in our latest report here or read on for the highlights.

1/ Social media compliance isn't enough

Just as consumers have been sharing opinions about restaurants and hotels online, so too are they sharing honest opinions about financial products and services.

These opinions are extremely public and mainly driven by personal experience. And it is an unfortunate truism that people are 50% more likely to share bad experiences on social media than good ones.

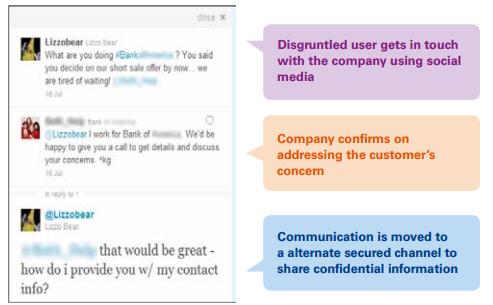

While it's plausible for an institution to write off one disgruntled customer, it's important to address the issue before the message hits 10,000 people.

When done correctly, social media monitoring can indicate any upcoming risks and mitigate the impact when they do occur.

In these situations research shows it's best to acknowledge customer feedback initially through social networks as it can potentially damage trust, and consequently the institution's image. Identify their sentiments, listen to their needs and respond to complaints on social.

People don't 'unsubscribe' as much on social channels as they would on e-commerce emails.

Then you can still decide to proactively use less public channels, such as direct phone calls or emails, to engage with customers in a way that is relevant, helpful and personal.

Fundamentally, the goal should be to interact and convert them from mere listeners to active participators or even brand advocates.

Every meaningful social conversation can be nurtured into a real relationship that can eventually become a direct revenue opportunity, positive word-of-mouth, or direct referral.

2/ Consumers want their banks to be where they are online

Compliance, security and privacy are still huge challenges for financial institutions when it comes to social.

On the one hand, they want to meet the demands and needs of their customers, in particular the younger generations who are used to doing everything in public light. On the other hand, banks have to do what's expected from a regulatory standpoint.

This is why most institutions have created Facebook, Twitter, YouTube or even Pinterest accounts, but don't allow customers to make payments, transfer money, or check their balances on those networks.

Instead, they offer these pages to educate, provide help and respond to questions in real time.

These channels are just a few examples. Companies should select the right mix based on the kind of customers talking to them (who?) and the information they want to share (what?).

There is no one-size-fits-all approach when it comes to being social.

3/ Social is not a silo

Despite being a late adopter of social media, today many financial services firms have observed the value in their social media engagements.

Nearly 70% of wealthy investors altered relationships with investment providers or reallocated investments based on the content they found on social media.

They've discovered that social media can have tremendous benefits for their businesses, whether through extensions of their PR, marketing, HR, sales or customer services team.

Almost every part of the business has a vested interest in social media monitoring. It is not about just one team, it's about the entire organisation.

At Brandwatch, we used to work with a lot of client's individual departments, but with each department running off and doing their own thing, there were huge inconsistencies within the organization.

In addition, people expect every financial institution to know who they are, regardless of which department they reach out to.

As in the case of other cross-department infrastructures such as CRM, financial institutions need a true social, interconnected infrastructure for optimizing client experience across channels, teams, departments, divisions and locations.

How else are they going to effectively manage conversations, campaigns, content and community at scale?

Operating in silos, where roles and responsibilities are blurred, will put the entire organization at a financial and reputational risk.

{kind=link}