"Because the purpose of business is to create a customer, the business enterprise has two-and only two-basic functions: marketing and innovation. Marketing and innovation produce results; all the rest are costs."

― Peter F. Drucker

One of the mistakes that successful companies make when faced with profound change in the business environment is to believe that their loyal customers will stay loyal, both to the brand and traditional business processes. Of course, building customer devotion is a necessity for brands nowadays, but leaders must recognize that today's strong brand loyalty offers no protection against significant changes in consumer expectations and behaviors.

This is an especially vital message now as we witness the birth and growth of the collaborative economy. No brand, regardless of existing consumer preference and loyalty, can avoid innovating to meet consumers' evolving expectations around sharing, renting, collective consumption and P2P (peer-to-peer) commerce.

I love the Drucker quote that leads off this blog post, although I would change one word, replacing "marketing" with "Customer Experience" (CX). At the time he said it, Drucker was referring to the old "Four Ps" model of marketing--product, price, place and promotion; nowadays, too many marketers are concerned with Promotion, leaving the other Ps to different parts of the organization. Nonetheless, what he says is that today's success is not enough; marketing and CX can create strong customer relationships today, but innovation is what creates strong customer relationships tomorrow.

Of course, studies demonstrate Drucker was correct. For example, in "The Living Company," Arie De Geus shares a study completed by Royal Dutch/Shell Group. Researchers examined similarities in companies that have existed since the nineteenth century. The study found that companies that enjoy long-term success share four attributes. Two do not pertain to innovation, but are important nonetheless--successful companies are fiscally conservative and have strong cultures with a firm sense of identity. The remaining two factors speak to the way innovation is baked into the core of their business:

- Successful companies are sensitive to their environment: "As wars, depressions, technologies, and political changes surged and ebbed around them, they always seemed to excel at keeping their feelers out, tuned to what-ever was going on around them." These companies "managed to react in timely fashion to the conditions of society around them."

- Successful companies are decentralized: De Geus later rethought the word and redefined it as "tolerant." He notes, "These companies were particularly tolerant of activities on the margin: outliers, experiments, and eccentricities within the boundaries of the cohesive firm, which kept stretching their understanding of possibilities."

|

| Source: Econsultancy |

History teaches us that today's brand strength furnishes no protection against the need to innovate. This has never been more true than today; while innovation has always been important, as the pace of change increases, the demand for business innovation grows. That companies today struggle with the quickening pace of innovation is apparent, as the average age of organizations in the S&P 500 has dropped from 60 years to less than twenty in the course of the past five decades.

We can examine what has occurred over the Internet era to see many obvious examples of companies that quickly failed despite very strong brand preference and customer loyalty. This loyalty meant little once the companies could not provide a product that met the changing needs and expectations of customers:

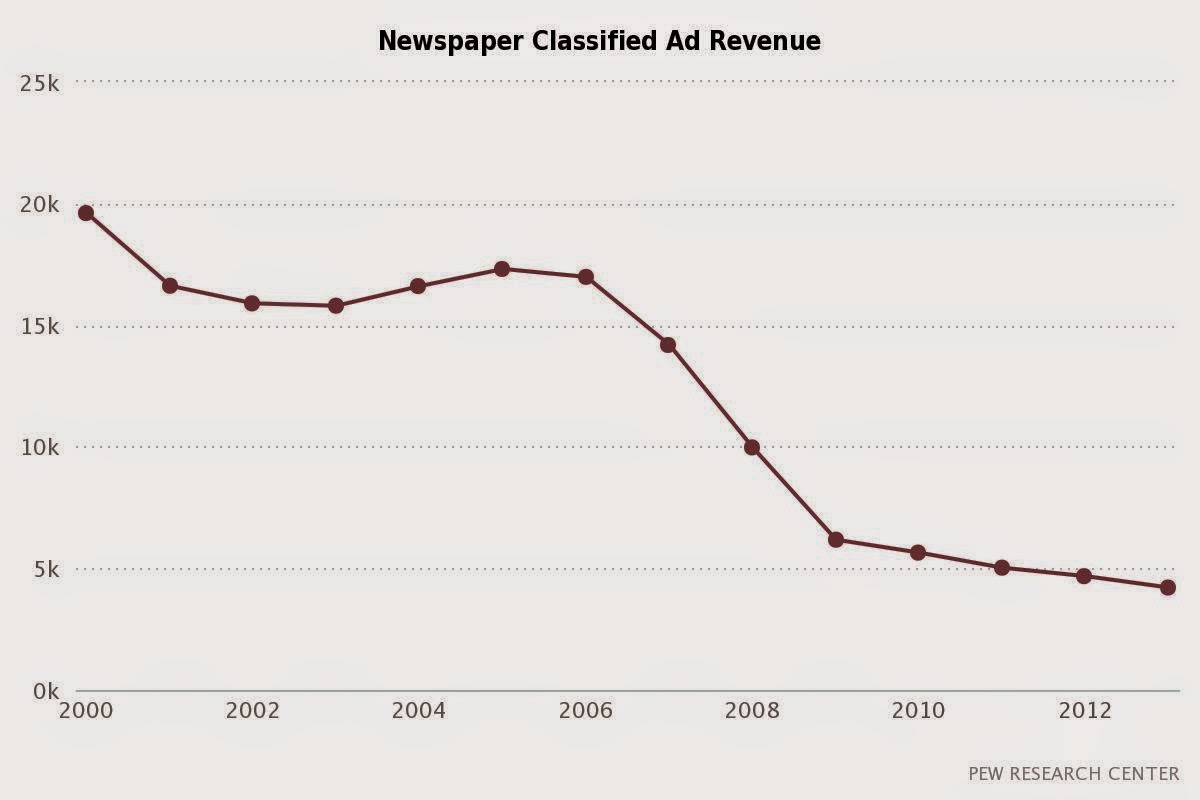

Newspapers: By the late 1990s, newspapers had seen an uninterrupted 40-year increase in both ad and circulation revenue. At the time, many in the news business saw the Internet as little risk given the high levels of subscriptions and trust people had in print media and low usage and trust consumers had for information on the Web. Newspaper were riding high with strong consumer perception and profitable business models. Then Craigslist and eBay launched P2P marketplaces, Monster created a digital job board and dozens of news sites like CNN.com and SFGate gained traction.

Source: Journalism.org

The result was the rapid destruction of newspapers' business models. Classified advertising dropped almost 80% in thirteen years and continues to fall today--down another 10.5% between 2012 and 2013. Circulation declines have not been as severe, but the trend has been consistently downward. In 2012, total daily newspaper circulation and total Sunday newspaper circulation were each equivalent to about one-third of U.S. households, down from around 55% in 2000.

Newspapers could have innovated with consumer behaviors, but instead they are playing catch-up. The recent release of the New York Times' digital strategy demonstrates just how much change newspapers still must undertake because they relied on existing customer loyalty and business models rather than on innovation. The question is if newspapers can adjust in time--in recent weeks Gannett, Tribune Company and E. W. Scripps, all empires built on the newspaper business, spun off their newspapers into separate businesses in order to reduce the earnings drag on their bottom line. The New York Times said the newspapers were "kicked to the curb" and questioned if they can survive (or if anyone will notice or care if they disappear).

Television Networks: Around 1980, the three big television networks had seen three decades of substantial growth in ratings, with viewers per season rising from 6 million in the early 1950s to more than 15 million around 1980. The launch of satellite and cable networks seemed a minor inconvenience, but it began a significant decline that only accelerated as the adoption of the Internet provided entertainment and video alternatives.

Source: Zap2It.com

The national networks have suffered a 50% decline in viewers by season over the last three decades. Today, there are even greater signs of change ahead; while traditional TV watching among older demographics has been steady in recent years, younger people are increasingly tuning out. In the past three years, Q1 TV viewing by 18-24-year-olds dropped by 4-and-a-half hours per week, or around 40 minutes per day.

Television networks did not adjust to the Internet age. People were recording and sharing their favorite TV shows via filesharing sites years before the networks would acknowledge the online demand for their content. The networks were slow to innovate, leaving openings for a slew of startups (many with dubious legal models) including Napster, The Pirate Bay and even YouTube (which in the early going was subject to great wrath from the networks for not preventing sharing of their IP.)

Today, less than ten years after YouTube's launch, its growing ad revenue is beginning to approach that of some cable and national TV networks. Meanwhile, a recent New York Times article notes that "no one really talks about the broadcast side anymore;" investors care more about the cable channels that the parent companies also own more than the big national networks. The enormous power and viewership of the national TV networks in 1980 could not prevent the 30-year decline of their business model as others innovated more rapidly.

Retail: By the late 90s, national retailers were riding high after decades of strong growth. Their enormous purchasing power had allowed them to shoulder smaller competitors out of the way. In 1948, single-location retailers accounted for 70.4% of US retail, but by 1997 this percentage had fallen to 39%; meanwhile, sales from chains with more than 100 locations grew from just 12.3% in 1948 to 36.9% in 1997. Worry about those tiny, money-losing online eretailers? Ha! Why would loyal customers begin to trust their credit card numbers and retail purchases online?!

Source: WSJ.com

Less then twenty years later, Borders, Circuit City and Linens 'n Things are gone. Other retailers--ones that not long ago possessed high levels of consumer trust and loyalty--are on life support, and few believe they can pull out of their death spirals. Radio Shack may not survive through the coming holiday season. And Sears Holdings, including both Sears and Kmart, have experienced constant declines in same-store sales over the past three years. (Since the beginning of 2011, the stock of Sears Holding has dropped almost 50%.)

I recently wrote about the lessons companies should learn from Borders' failure, but here is perhaps the most surprising fact about the chain's demise: Just six months before the company filed for Chapter 11 bankruptcy, Forrester declared Borders the top company in the nation in its Customer Experience Index (CxP). The research firm surveyed consumers for opinions on their experiences with over 150 brands, and customers put Borders at the top. At the very same time that Borders had the strongest customer perception in the country, it failed.

.gif)

"The people who work within these industries or public services know that there are basic flaws. But they are almost forced to ignore them and to concentrate instead on patching here, improving there, fighting the fire or caulking that crack. They are thus unable to take the innovation seriously, let alone to try to compete with it. They do not, as a rule, even notice it until it has grown so big as to encroach on their industry or service, by which time it has become irreversible. In the meantime, the innovators have the field to themselves."

― Peter F. Drucker

customer loyalty / shutterstock

{kind=link}